How to Build an Investor Ready Cap Table for Indian Startups

Building an investor ready cap table is the foundation of successful fundraising for Indian startups. Yet, most founders treat their capitalization table as an afterthought—until it costs them a term sheet or millions in exit proceeds.

After advising dozens of Indian startups through seed rounds, Series A negotiations, and M&A transactions, I’ve seen how cap table decisions in the earliest days shape outcomes years later. In India, ESOP compliance under the Companies Act and SEBI regulations adds layers of complexity that make proper cap table management even more critical. This guide shows you exactly how to build a cap table that attracts institutional investors and protects founder value.

What Makes a Cap Table “Investor Ready”?

An investor ready cap table goes beyond basic ownership tracking. It demonstrates:

- Clean ownership structure: Clear documentation of who owns what, with all instruments properly recorded—equity shares, CCPS, convertible notes, and option grants under SEBI-compliant ESOP schemes.

- Founder alignment: Vesting schedules for founders are typically 3-4 years with one-year cliff. These reflect founders’ commitment and protecting against early departures that create dead equity.

- Appropriate dilution levels: Founders maintaining meaningful ownership ~60% post-seed, 40-50% post-Series A. It keeps them motivated through the long journey ahead.

- Regulatory compliance: For Indian startups, this means proper board resolutions, shareholder approvals, and Companies Act 2013 Section 62(1)(b) compliance for all equity issuances. If the equity has been raised from overseas, it also means proper FEMA compliances.

- ESOP infrastructure: A properly sized option pool (typically 15-18%) with merchant banker valuations for Indian tax compliance and clear documentation under Companies Act Rule 12.

When institutional investors review your cap table during due diligence, they’re evaluating whether you understand equity management. Moreover, it gives them a sense whether investing in your company will create complications down the road.

The India Context: ESOP and Regulatory Compliance

Indian startups face unique regulatory requirements that many founders underestimate.

- Companies Act 2013 Requirements

Section 62(1)(b) authorizes ESOP schemes but requires special resolution by shareholders, detailed disclosure, and compliance with prescribed rules. This isn’t optional paperwork—it’s the legal foundation for your employee equity program.

Rule 12 of the Companies (Share Capital and Debentures) Rules, 2014 governs employee stock option schemes, specifying eligibility criteria and vesting requirements. Notably, promoters and directors holding over 10% equity are not eligible for ESOPs except in DPIIT-recognized startups for 10 years from incorporation.

- SEBI Regulations for Listed Companies

If you’re planning an IPO, SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021 replaced earlier 2014 regulations and provide a comprehensive framework covering ESOPs, RSUs, SARs, and other equity instruments.

Recent changes make this even more relevant. In June 2025, SEBI amended regulations to permit promoters to hold and be granted share-based benefits including ESOPs, which previously had to be liquidated before IPO. This aligns Indian regulations with international practices and strengthens founder retention.

- Tax Implications

Section 17(2)(vi) treats ESOP perquisite as salary income, with the perquisite value calculated as fair market value at exercise minus exercise price paid. Timing matters: for eligible startup companies, employees can defer tax on ESOP perquisites for up to 48 months from the end of the assessment year in which shares are allotted, provided certain conditions are met.

Understanding these rules isn’t just about compliance—it’s about structuring your equity program to be competitive in hiring while managing cash burn.

What Investors Look for When Reviewing Your Cap Table

Founder Ownership and Vesting in the Cap Table

Institutional investors expect founders to collectively own 50-60% after seed or Series A. When we see founders with 15-20% at seed stage, it signals they either gave away too much equity too early or had co-founder departures without proper vesting.

Ideally founder’s equity should be subject to vesting, even if they’ve been working on the company for two years pre-incorporation. This protects everyone. The standard is four years with a one-year cliff, meaning nothing vests in the first year, then 25% vests on the one-year anniversary and so on.

Investor Concentration: Quality Over Quantity

The concentrated cap table: One client raised ₹1.5 crore from a single institutional seed fund that took 18% equity. When they raised Series A eighteen months later, the diligence process took three weeks. The cap table fit on one page. There was one institutional reference to check. The company raised ₹6 crore at a strong valuation, and founders retained 52% ownership.

The fragmented cap table: Another client raised ₹1.2 crore from 8-10 small investors including NRIs over rolling closes spanning nine months. Each investor had slightly different terms. Some had valuation caps on convertibles ranging from ₹4 crore to ₹9 crore, others had discount rates between 15-25%. When they attempted Series A, potential leads found it impossible to model the fully diluted ownership because conversion terms varied so widely. After five months of fundraising struggles, they accepted a down round with harsh terms. Founder ownership was crushed to 31% post-Series A.

The lesson: Five strategic angels who each invest ₹20 lakhs and can make valuable introductions are infinitely more valuable than twenty-five ₹5 lakh checks from passive investors.

Dead Equity Red Flags

Dead equity—significant ownership held by people no longer contributing. It is one of the fastest ways to kill a fundraising round. Common examples:

- Departed co-founder still holding 25-30% without vesting

- University tech transfer office holding 15% post-spinout

- Advisors with 2-3% for making a few introductions

- Family members who invested early but provide no ongoing value

The solution of a buyback negotiation can consume months, legal fees and uneasiness with potential investors.

Option Pool Sizing

Not having an ESOP pool is not an option. The key employees need incentive to stay and build the company. For VC-backed companies, ESOP pools and vesting schedules are often negotiated at the term sheet level. Investors typically expect 15-18% allocated pre-Series A.

The negotiation point: Does the option pool expansion happen pre-money (diluting only founders) or post-money (diluting all shareholders proportionally)? Investors almost always push for pre-money. Founders should understand this dynamic and negotiate accordingly.

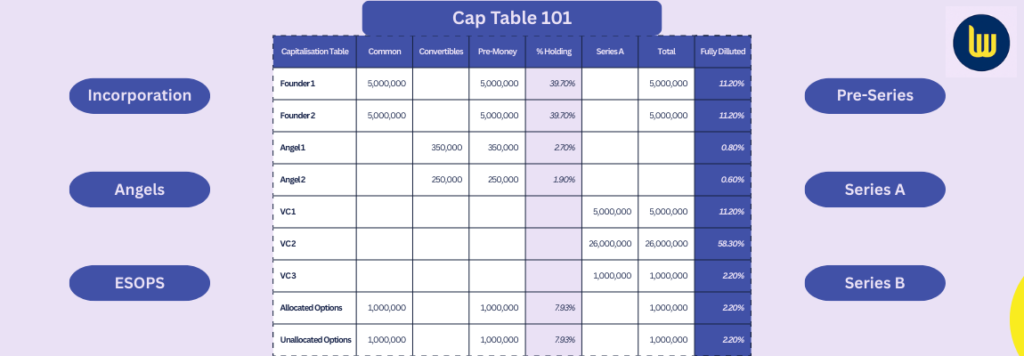

Building Your Cap Table: Stage-by-Stage Framework

Incorporation Stage: Set the Foundation

Create your cap table the day you incorporate as a private limited company. Issue founder common shares with four-year vesting and one-year cliff.

Allocate founder equity based on realistic assessment of contribution, commitment, and value. Unequal splits are acceptable if justified—60/40 or 70/30 splits can work if one founder is full-time CEO and another is CTO joining part-time initially. Document your reasoning.

What’s not acceptable: A handshake agreement or “we’ll figure it out later.” That creates disputes when the company has value worth fighting over.

Angel and Seed Stage: Discipline Over Desperation

If you raise before institutional investors enter, be ruthless about terms and investor selection.

- Use standard instruments: Simple convertible notes or SAFE equivalents work in India. Don’t create custom structures to close one investor—they’ll confuse the next ten.

- Set terms once, apply uniformly: Decide on your valuation cap and discount rate, then apply them to everyone in that round. Do not negotiate individually.

- Be selective: Choose angels who bring strategic value—customer introductions, domain expertise, future investor connections. In Indian fintech and consumer internet sectors, the right five angels can open more doors than twenty-five passive investors.

- Limit special rights: Pro-rata participation rights, board observer seats, and extensive information rights should be reserved for lead investors writing ₹50 lakhs minimum, not extended to every ₹5 lakh angel.

- Document everything: Maintain perfect records with board approvals (Form MGT-14), shareholder resolutions, share certificates, and Register SH-6 for ESOPs.

Institutional Rounds: Long-Term Partnership Decisions

When venture capital enters, you’re choosing long-term partners who’ll be on your board and cap table for 5-7 years minimum.

Institutional Investor selection criteria:

- Track record of supporting companies through difficult periods

- Value-add beyond capital (network, operational expertise, strategic guidance)

- Follow-on capacity to support subsequent rounds

- Alignment on exit timeline and return expectations

- Reference checks with founders they’ve backed, especially companies that struggled

Pay attention to these terms

Term sheet negotiation priorities:

The economic terms that matter most:

- Valuation: Higher pre-money means less dilution, but an excessively high valuation creates problems if growth doesn’t justify it in the next round.

- Liquidation preference: Fight hard to keep this at 1x non-participating. Participating preferred stock with 2x or 3x liquidation preferences heavily favor investors in moderate exit scenarios.

- Anti-dilution provisions: Weighted average is standard and fair. Full ratchet should be avoided except in dire circumstances—it punishes founders severely if the next round is a down round.

- Option pool: Negotiate whether the pool expansion happens pre-money (founders bear all dilution) or post-money (all shareholders dilute proportionally).

The control terms that matter the most:

- Board composition: Maintain balanced representation. A typical Series A board is two founders, two investors, one independent. This prevents either side from making unilateral decisions while ensuring the company can act decisively.

- Protective provisions: Standard investor protections are reasonable—approval rights on selling the company, raising debt, changing the charter. Be wary of provisions giving investors veto power over ordinary operations.

- Drag-along rights: These ensure all shareholders must participate in a future sale if a supermajority (typically 75-85%) approves it, preventing small shareholders from blocking exits.

The Cost of Cap Table Mistakes

Case Study 1: The Non-Strategic Single Investor

I worked with a consumer tech company that raised their seed round (₹2 crore for 20%) from a single investor with deep pockets but no strategic value in their sector. The investor viewed this as a passive financial investment, not a partnership.

For the first twelve months, this seemed fine. The company had cash, was building product, acquiring users. But when they needed additional round and introductions to Series A investors, their sole investor couldn’t help. They had no network or expertise in the sector, and no interest in anything beyond financial returns. They did not understand the pivots, which the company was required to do in the high-growth sector.

When the company headed for a new investor, it was hard to get one, as the current investor was non-strategic and the new investor did not want to share the Board with the existing investor.

The company had to scramble for bridge financing at distress terms and eventually could not onboard any new investor.

The lesson: Having a strategic investor at the start is more crucial than financial investor with no understanding of the business and its challenges.

Case Study 2: The Crowded Angel Round

I’ve advised multiple startups in fintech, consumer internet, and social apps, which made the same mistake: raising from too many small investors.

One social app startup raised ₹1.8 crore from 15 different angels. Many wrote ₹3-7 lakh checks. Moreover, some were on convertible notes and some others on priced rounds.

The problems compounded:

- Coordination nightmare: For holding General Body Meetings, some investors expected detailed metrics, others wanted board-level summaries in their standard formats. Founder time was consumed managing investor communications instead of building product.

- Conversion complexity: With instruments converting at different caps and different discount rates, modeling the fully diluted cap table became nearly impossible. Different angels had different expectations about what their ownership percentage would be post-conversion.

- Blocking minority issues: Two angels did not accept the valuation at Series A, as they expected the value to be multi-fold.

- Due diligence delays: During Series A diligence, the lead investor needed confirmation from all shareholders about ownership, rights, and any side agreements. Three angels didn’t respond to emails for weeks. One angel demanded to review the new term sheet and sent questions through his lawyer, adding six weeks to the process.

After seven months of fundraising attempts, the company eventually raised much lower capital at a lower valuation—below what they’d hoped for.

What they should have done: Raised the same ₹1.8 crore from 3-5 high-quality angels, set standard terms at the beginning, closed within 4-6 weeks maximum, and spent the saved time building their business instead of managing investor complexity.

Practical Cap Table Management for Indian Startups

Poor documentation doesn’t just create confusion—it creates legal risk that surfaces during due diligence and can kill financing rounds.

Software vs. Spreadsheets

- Spreadsheets work when you have three founders and zero employees. They fail catastrophically when you have 20 option holders, convertible instruments converting at different caps, and CCPS with liquidation preferences.

- For Indian startups, consider platforms that handle local compliance:

- Qapita offers SEBI-regulated workflows and merchant banker valuations with Companies Act compliance,

- EquityList specializes in Indian regulatory requirements including dematerialization services.

- The cost is trivial—often ₹30,000-50,000 annually for early-stage startups—compared to the risk of errors that could cost millions in misunderstood ownership or compliance violations.

Compliance Checklist

- Proper company incorporation under Companies Act 2013

- Board resolution and special shareholder resolution for ESOP scheme

- Merchant banker or registered valuer report for fair market value at grant and exercise

- Form MGT-14 filed for board resolutions within 30 days

- Register SH-6 maintained with grant, vesting, exercise, and cancellation records

- Form PAS-3 filed for share allotment within 30 days

- For foreign investors: FEMA compliance and RBI reporting

- For employees with foreign parent company ESOPs: Form OPI filed semi-annually through authorized dealer bank

Documentation that matters

- Board approval with proper quorum and meeting minutes

- Shareholder approval where required (special resolutions for ESOPs, preferential allotment)

- Share certificates issued and recorded

- Vesting schedules documented and tracked

- Option grant letters with exercise prices, vesting terms, and exercise windows

- Convertible instrument agreements with clear conversion mechanics

- Shareholders agreement governing rights and obligations

- Articles of Association amendments where equity classes change

Frequently Asked Questions

How do I know if my cap table is investor ready?

An investor ready cap table meets these criteria:

- You can produce fully diluted ownership calculations in under 30 minutes

- Every equity grant has proper documentation with board approvals

- All vesting schedules are tracked and current

- Convertible instruments have clear conversion mechanics documented

- For Indian startups, all Companies Act and SEBI filings are current

- You can model exit scenarios showing proceeds distribution by stakeholder class

If you can't quickly answer "who owns what percentage after all options vest and all convertibles convert," your cap table needs work.

What's the right ESOP pool size for an Indian startup?

Pre-Series A: 15-18% is standard. This should support 18-24 months of hiring based on your growth plan.

Series A and beyond: Refresh to maintain 15-20%, or expand to 20% if you're in a competitive hiring market (AI/ML, product management, senior engineering in Bangalore/NCR).

Remember: For VC-backed companies, ESOP pools and vesting schedules are often negotiated at the term sheet level. The size directly impacts founder dilution, so this becomes a key negotiating point.

Should I use convertible notes or priced equity rounds?

For early-stage rounds (angel/seed in India), convertible notes or SAFE-equivalent instruments work well because:

- Faster to execute (no valuation negotiation required)

- Less legal expense (standard documentation)

- Defers valuation discussion to institutional round

For institutional rounds (Series A+), priced equity rounds are standard because:

- Investors want preferred stock with clear rights and preferences

- Valuation needs to be established for fund reporting

- Board seats and governance provisions require formal equity classes

Never create custom hybrid structures. Use standard instruments that future investors will understand.

How do I fix a messy cap table?

Options include:

Buyback dead equity: Negotiate with departed founders or inactive stakeholders to repurchase their shares at fair value.

Consolidate small positions: Offer secondary liquidity to small angels, with new investors or the company buying their positions to simplify the cap table.

Recapitalization: In severe cases, create a new entity with clean structure and roll forward only active stakeholders. This is expensive and time-consuming but sometimes necessary.

Prevention is infinitely better than these cures. Start clean and stay clean.

What happens to my cap table in an acquisition?

Your cap table determines exactly how proceeds distribute. The waterfall accounts for:

- Liquidation preferences (1x non-participating means investors get 1x their investment or their ownership percentage of proceeds, whichever is higher)

- Participation rights (participating preferred gets preference amount plus share of remaining proceeds)

- Vested vs. unvested option treatment

- Escrow or earnout allocations

In a ₹50 crore acquisition, the difference between clean terms (1x non-participating preferred) and investor-heavy terms (2x participating preferred with full ratchet anti-dilution) can be ₹10-15 crore in founder proceeds.

This is why term sheet negotiation matters so much.

How do I manage cap table with employees across multiple Indian states or internationally?

For multi-location Indian companies:

- Create one topco-level option pool for consistency

- Use country-specific sub-plans for compliance

- Ensure compliance with Ind AS 102 for accounting treatment

- Work with local legal counsel for state-specific labor laws

For international employees:

- For foreign parent ESOPs granted to Indian employees, file Form OPI semi-annually through authorized dealer bank

- Understand withholding obligations across jurisdictions

- Consider Double Tax Avoidance Agreements (DTAA) for employees

- Use cap table software with global capabilities

Final Thoughts: Your Cap Table as Strategic Asset

Your cap table is not administrative paperwork. It’s a strategic decision document that shapes every fundraising conversation, every hiring negotiation, and ultimately your exit outcome.

The decisions you make at incorporation—implementing founder vesting, allocating equity thoughtfully, choosing your first investors carefully—compound through every subsequent round. A clean cap table accelerates fundraising because investors see discipline and thoughtfulness. A messy cap table raises questions about what other aspects of your business might be poorly managed.

For Indian startups, the regulatory overlay—Companies Act compliance, SEBI regulations, merchant banker valuations, ESOP taxation—makes this even more critical. Getting these foundations right from Day 1 prevents expensive problems down the road.

Build your cap table with the same rigor you apply to your product development, your financial model, and your go-to-market strategy. Choose your investors as carefully as you choose your co-founders. Document everything scrupulously. Model dilution scenarios proactively.

And never make equity decisions when you’re desperate for capital—that’s when the most costly mistakes happen.

To discuss your cap table’s unique characteristics with Deepti Beri, the founder of BizWise Advisors, and understand what makes sense for your business:

1 Comment

This is insightful. It has been comprehended well and gives companies and boards the right direction. Fractional CFO as a concept is catching up and paying for intellectual capital serves in the long term